Have you ever checked your bank statement and seen a mysterious “ACH” transaction? You probably thought, “What does ACH mean in banking?” 🤔 Don’t worry this isn’t some secret code.

ACH is one of the most common ways money moves between banks in the U.S., and understanding it can save you confusion and even missed payments.

Quick Answer:

ACH means “Automated Clearing House.” It’s a secure, electronic funds transfer (EFT) system that allows banks to move money efficiently, whether it’s direct deposits, bill payments, or other transfers.

What Does ACH Mean in Banking? 🧠

ACH is short for Automated Clearing House, a network that processes electronic payments between U.S. banks. It’s used for:

- Direct deposits of paychecks

- Recurring bill payments like utilities or subscriptions

- One-time money transfers between bank accounts

Example Sentence:

“My rent was paid via ACH, so the landlord got the money directly from my account.”

In short: ACH = Automated Clearing House = electronic bank transfer system ✅

Authority Note: ACH transfers are governed by NACHA (National Automated Clearing House Association) and regulated by the Federal Reserve, ensuring they’re safe and secure.

How ACH Transfers Work Step by Step 🏦

Here’s a quick step by step guide to help you understand ACH transfers:

- Initiate Transfer: You authorize your bank to send money (for bills, payroll, or transfers).

- Bank Submits ACH Entry: Your bank sends a request through the ACH network.

- Processing: The network batches and processes the transactions.

- Receiving Bank Credits Account: The recipient’s bank receives the payment and credits the account.

- Confirmation: Both sender and receiver are notified of the successful transfer.

Example:

“My employer uses ACH to deposit my salary. On payday, the money hits my account automatically without any action on my part.”

Where Is ACH Commonly Used? 📱

ACH is widely used in U.S. banking, especially for recurring or one-time payments:

- 💻 Online banking portals — viewing ACH transactions

- 📲 Payment apps (PayPal, Venmo) — mentions ACH transfers

- 🏦 Employer payroll systems — via ACH direct deposit

- 📧 Bank notifications — “Your ACH payment of $500 has cleared”

Tone: formal and professional; rarely casual.

ACH vs Other Payment Methods: Comparison Table 🔄

| Payment Method | Speed | Cost | Use Case | Pros | Cons |

| ACH Transfer | 1–3 business days | Usually free | Payroll, bills | Secure, automated | Not instant |

| Wire Transfer | Same day | $15–$30 | Urgent payments | Instant, reliable | Expensive |

| EFT | 1–3 days | Usually free | Generic electronic transfers | Flexible | Slower than wire |

| Zelle | Minutes | Free | Peer-to-peer | Instant | Limited to participating banks |

| PayPal/Venmo | Minutes | Free/$2.99 | Personal payments | Instant & easy | Can incur fees for bank transfers |

Examples of ACH in Conversation 💬

Here are realistic ways people might refer to ACH:

A: “Did my paycheck arrive?”

B: “Yep, ACH deposit hit my account today 😎”

A: “I paid the rent.”

B: “Got it! The ACH transfer worked ✅”

A: “How long does it take?”

B: “Usually 1–3 days. ACH processing time varies by bank ⏳”

A: “Can I reverse an ACH payment?”

B: “Yes, but only for errors or fraud. Contact your bank.”

A: “I want instant transfer.”

B: “ACH is not instant. Try wire transfer or Zelle instead.”

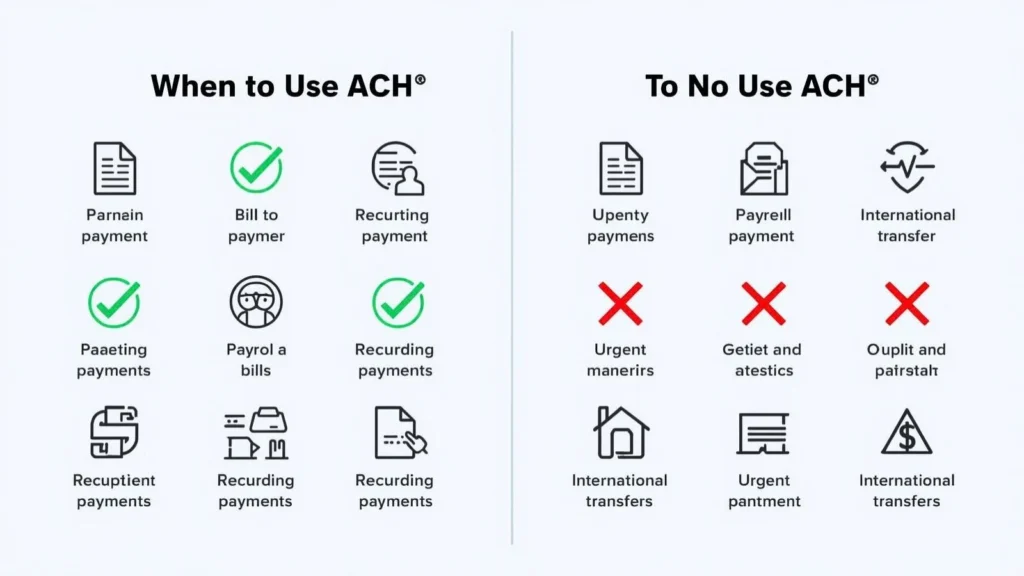

When to Use and When Not to Use ACH 🕓

✅ When to Use:

- Direct deposit for salaries

- Paying bills electronically

- Recurring or scheduled transfers

- Moving money between your accounts

❌ When Not to Use:

- Urgent or same-day payments (ACH is slower than wire)

- International transfers (ACH is U.S.-only)

- Situations requiring informal peer-to-peer slang

Quick Context Table:

| Context | Example Phrase | Why It Works |

| Friend Chat | “Sent via ACH, should arrive tomorrow 😄” | Casual & informative |

| Work Chat | “Payroll processed via ACH direct deposit” | Professional & clear |

| “Your ACH transaction has been completed successfully” | Formal & precise |

Similar Banking Terms or Alternatives 🔄

| Term | Meaning | When to Use |

| Wire Transfer | Instant bank-to-bank transfer | Urgent, large payments |

| Direct Deposit | Employer sends salary directly | Payroll & recurring income |

| EFT | Generic electronic transfer | Any online banking transfer |

| Zelle | Fast P2P transfer | Quick personal payments |

| PayPal/Venmo | Peer-to-peer digital payments | Casual money transfers |

FAQs About ACH ❓

Q1: Is ACH safe?

Yes, ACH transfers are secure and regulated by NACHA and the Federal Reserve.

Q2: How long does an ACH transfer take?

Typically 1–3 business days, but same-day ACH is available for some banks.

Q3: Can I reverse an ACH payment?

Yes, but only in cases of errors or fraud.

Q4: Is ACH international?

No, ACH transfers work only in the U.S. For international payments, use wire transfer.

Q5: Does ACH cost money?

Usually free for personal use, though some banks may charge fees for certain ACH transactions.

Q6: ACH vs Wire Transfer — which is better?

- Use ACH for recurring or non-urgent payments (free, automated).

- Use wire transfer for urgent or large amounts (instant but costs more).

Conclusion 🏁

Now you know what ACH means in banking and how it works. ACH, or Automated Clearing House, is a secure and reliable electronic funds transfer system widely used for direct deposits, bill payments, and account transfers.

By understanding ACH payments, ACH transfers, and ACH processing times, you can manage your money confidently.

Next time you see an ACH transaction, you’ll know exactly what it is and why it’s faster and safer than writing a check!

Authority Reminder: NACHA and Federal Reserve ensure ACH transfers are secure and standardized across U.S. banks.

Andrew Michael is a visionary thinker and passionate creator, focused on turning bold ideas into real-world impact. His creativity and dedication inspire others to grow, achieve, and make a difference.

Leave a Comment